I was there when the first teams went to Bangalore.

Around 2000, offshoring wasn't yet a McKinsey slide deck everyone copied. It wasn't the default play in every PE and public equity value creation plan. I was at the beginning of my career, a junior engineer watching it happen from the inside, part of early teams being set up in India, observing firsthand how the model was born. Simple logic: skilled engineers in Bangalore at a fraction of Western salaries. The math was obvious. The results were good enough.

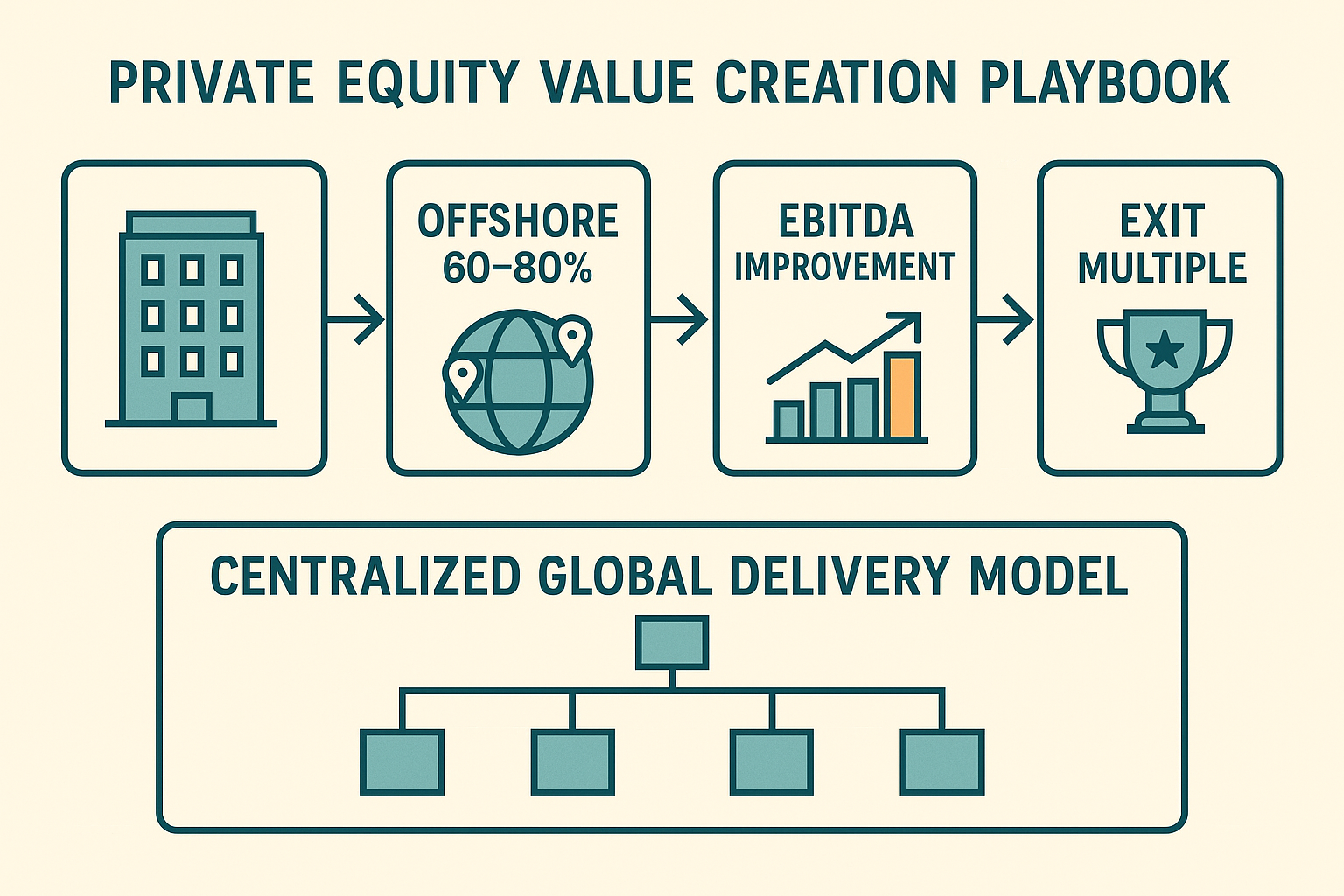

Over the next twenty years, I ran the play myself, many times. I hired hundreds of engineers in Bangalore. I optimized the hiring model, the delivery model, the operating model structure. I built centralized Global Delivery Models out of what had previously been fragmented, decentralized offshore pockets scattered across business units, each running their own vendor relationships, their own processes, their own management overhead. Centralizing that into a single global delivery model was where the real economies of scale lived, and I extracted them.

I know exactly how this model works. Which means I know exactly what's ending. And why.

Two Investors, One Bet

The offshoring machine didn't run on one type of capital. It ran on two.

Private equity had the cleanest version. Acquire companies. Identify the tech teams as a cost center. Offshore 60-80% of engineering to India, Eastern Europe,South America. Pocket the labor arbitrage as EBITDA improvement. Exit at a higher multiple. Nearly every PE-backed tech company in the last two decades went through some version of this. The value creation deck always had that slide. Always. "Optimize engineering costs through offshore delivery." It was so standard it was boring. Nobody questioned it. Up to 70% cost savings, reliable as clockwork.

But the smart operators didn't stop at the arbitrage. They consolidated. Fragmented, decentralized offshore teams across business units were expensive to run, hard to manage, and full of redundancy. The real EBITDA lever was centralizing that chaos into a single Global Delivery Model: one governance structure, one set of processes, one management layer across all geographies. Economies of scale on top of already cheap labor. That's where the 35-point gross margin improvements actually came from.

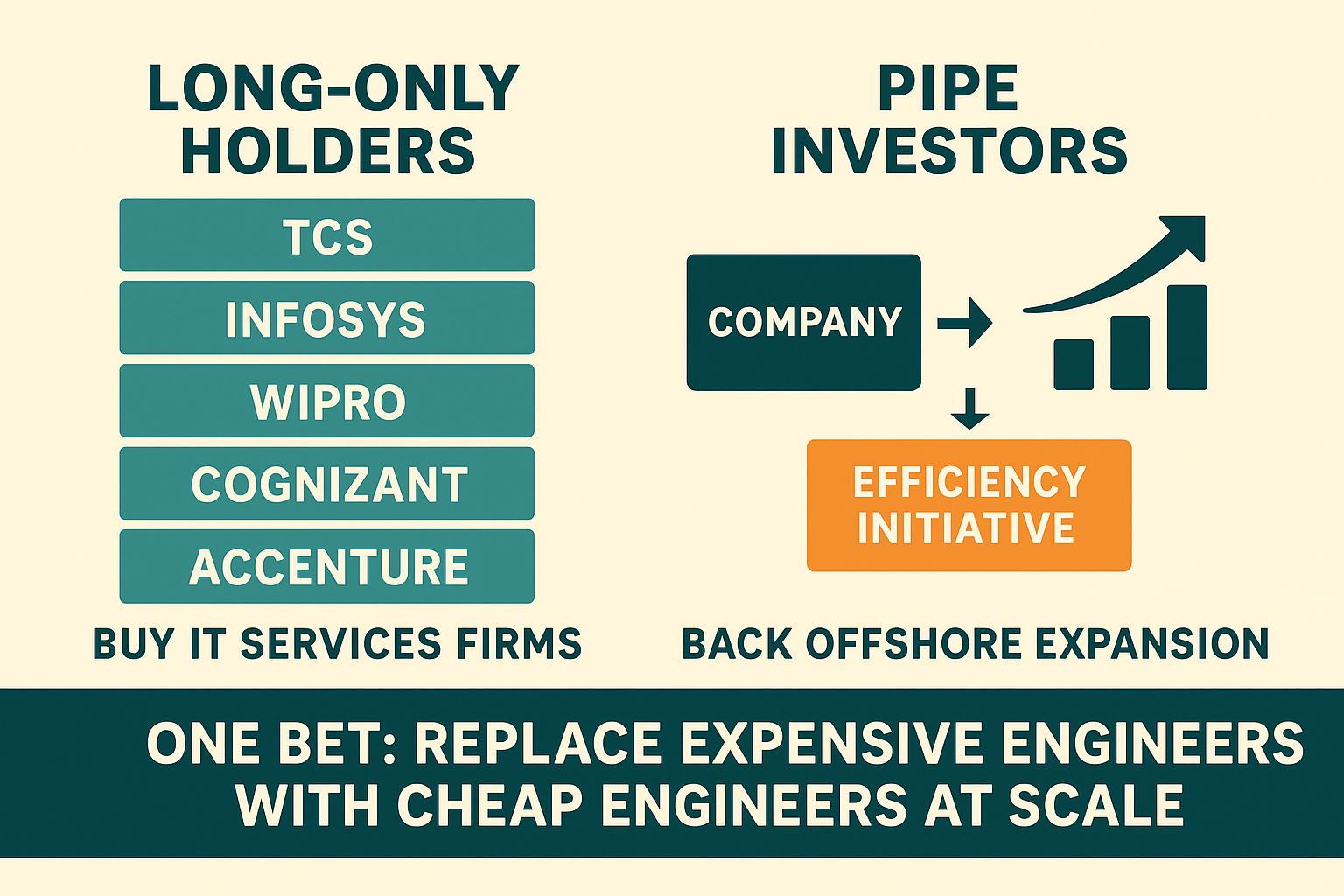

Public equity ran the same thesis, different wrapper. Long-only holders loaded up on IT services firms directly: Infosys, TCS, Wipro, Cognizant, Accenture or building their own development center. Companies whose entire revenue model IS the arbitrage, packaged as managed services. They already had the Global Delivery Model built. You weren't buying individual cheap engineers. You were buying industrialized, at-scale delivery of cheap engineers. PIPE investors backed public companies announcing "operational efficiency initiatives" and "global delivery model optimization." Stock pops on the news. What it actually means: we're replacing $150/hour engineers with $35/hour engineers and calling it strategy.

I've looked at PIPE deals where the entire investment thesis was margin expansion driven by offshore delivery optimization. The deck says "global delivery model." The financial model shows 35-point gross margin improvement over three years. And underneath all of it is just: we're replacing expensive engineers with cheap engineers at scale. That story worked for a decade.

Two different positions, two different return profiles, one underlying bet: Western engineers cost too much. Eastern engineers cost less. And at sufficient scale, the economics compound. Simple math, reliable returns. For thirty years, the bet paid off beautifully.

It's not paying off anymore.

The $600B Empire Built on a Wage Gap

Let's be precise about what we're talking about. The global IT outsourcing market hit roughly $600B in 2025. The offshore segment holds about half of that revenue. The Big Five built empires on one simple premise: humans in Bangalore cost less than humans in San Francisco.

TCS: 582,000 employees, $29B in revenue. Infosys: 300,000+. Wipro: 250,000. Cognizant: $21B revenue. Accenture: $22B in bookings last quarter alone. Together, they employ well over a million people. The business model is elegant in its simplicity. Take work that costs $X onshore. Deliver it for $X/3 offshore. Charge the client $X/2. The margin lives in the gap between those numbers.

But IT services is just the visible part of the iceberg. The labor arbitrage thesis runs far deeper than software development. PE firms and public companies used the same playbook across manufacturing, customer support, back-office operations, financial services ops, healthcare administration. The business process outsourcing market alone is worth hundreds of billions more. Offshoring wasn't a tech industry phenomenon. It was a capital allocation strategy that touched every sector where humans did repeatable work.

And then there's the layer most people forget: the staffing and contracting companies. Randstad Tech, Hays, ManpowerGroup's tech division. They don't do the work themselves. They place contractors and bill hourly. They're the intermediaries' intermediaries. When a PE-backed portfolio company needs 40 Java developers in Hyderabad, these firms find them, onboard them, handle payroll, and take their cut. An entire ecosystem of companies whose business model depends on demand for human technical labor remaining high and fragmented.

System integrators too. Capgemini, Atos, DXC Technology. Same exposure as TCS and Infosys, different branding. Whether you call it "IT services," "systems integration," or "digital transformation consulting," the revenue model underneath is identical: bill for human hours, deliver those hours at the cheapest possible cost.

The total blast radius isn't a $600B IT outsourcing market. It's a multi-trillion-dollar global labor arbitrage ecosystem spanning every industry where humans perform structured, repeatable tasks. That's what's in the crosshairs.

The Market Already Knows

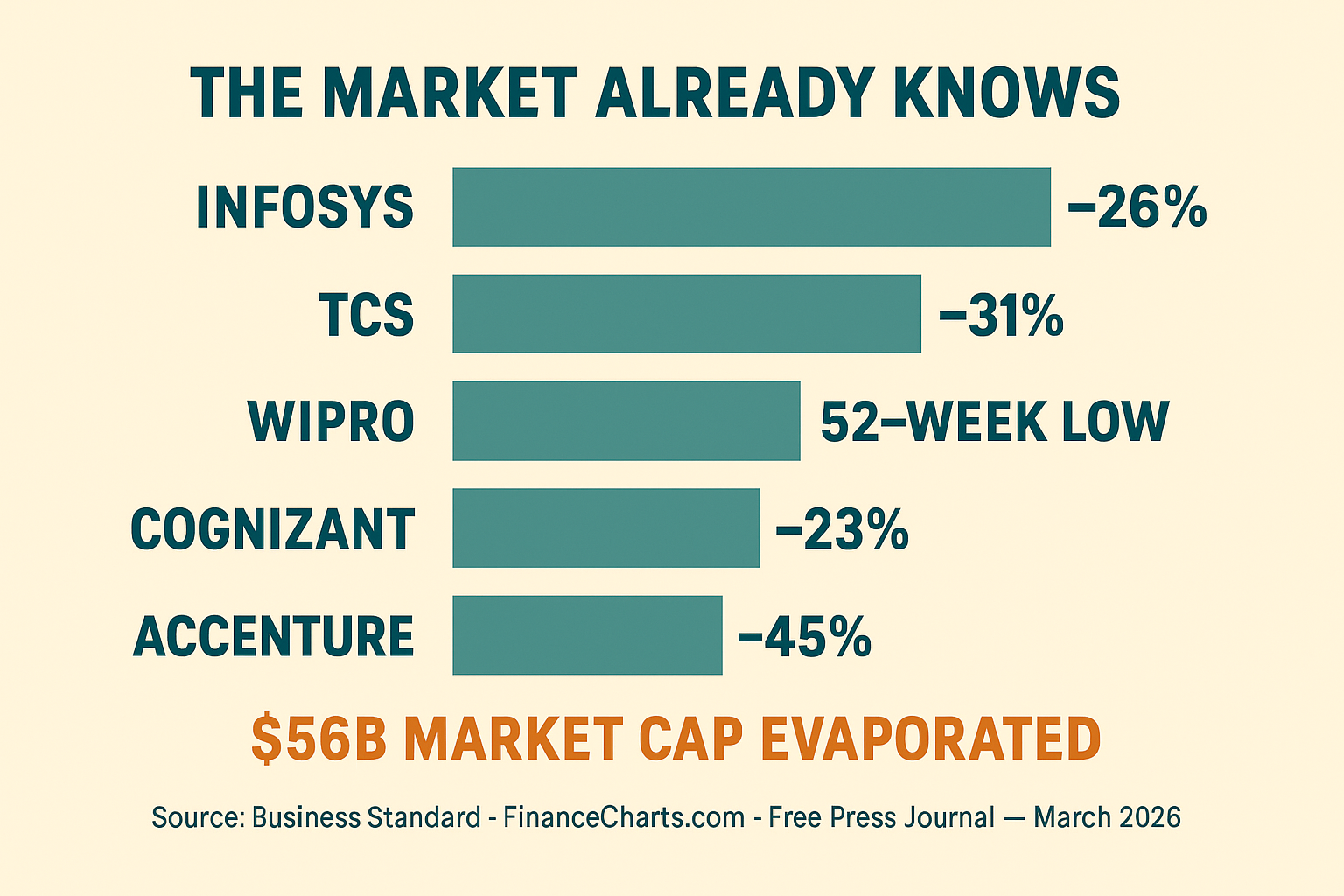

The stocks tell the story before the earnings calls do. As of March 2026:

Infosys: down 26% year-to-date, hitting its lowest level since December 2020 on AI disruption fears (Business Standard, March 2026). TCS: down 31% from January 2025 highs (Free Press Journal, January 2026). Wipro: trading near 52-week lows. Cognizant: down 23% in 2025, touching $63.81. Accenture: down 45% from its February 2025 peak, despite posting record bookings.

$56 billion in market cap evaporated from Indian IT stocks alone. Not on missed earnings. Not on lost contracts. On the market's recognition that the model underneath these companies has an expiration date.

As I wrote in The Agentic-Native Paradigm for Investors, we watched $2 trillion in SaaS market cap evaporate as the market repriced the entire category. Different victim, same killer. The structural pattern is identical. Capital that flowed into one paradigm for decades suddenly recognizes the paradigm is breaking. And capital doesn't wait for the companies to confirm it. Same feeling as watching SaaS multiples compress. Different ticker symbols, same underlying thesis dying in public.

Any public equity investor who loaded up on these names, any PIPE investor who backed "operational efficiency" narratives built on offshoring, is watching those margin stories unravel in real time.

Why Agents Kill the Arbitrage

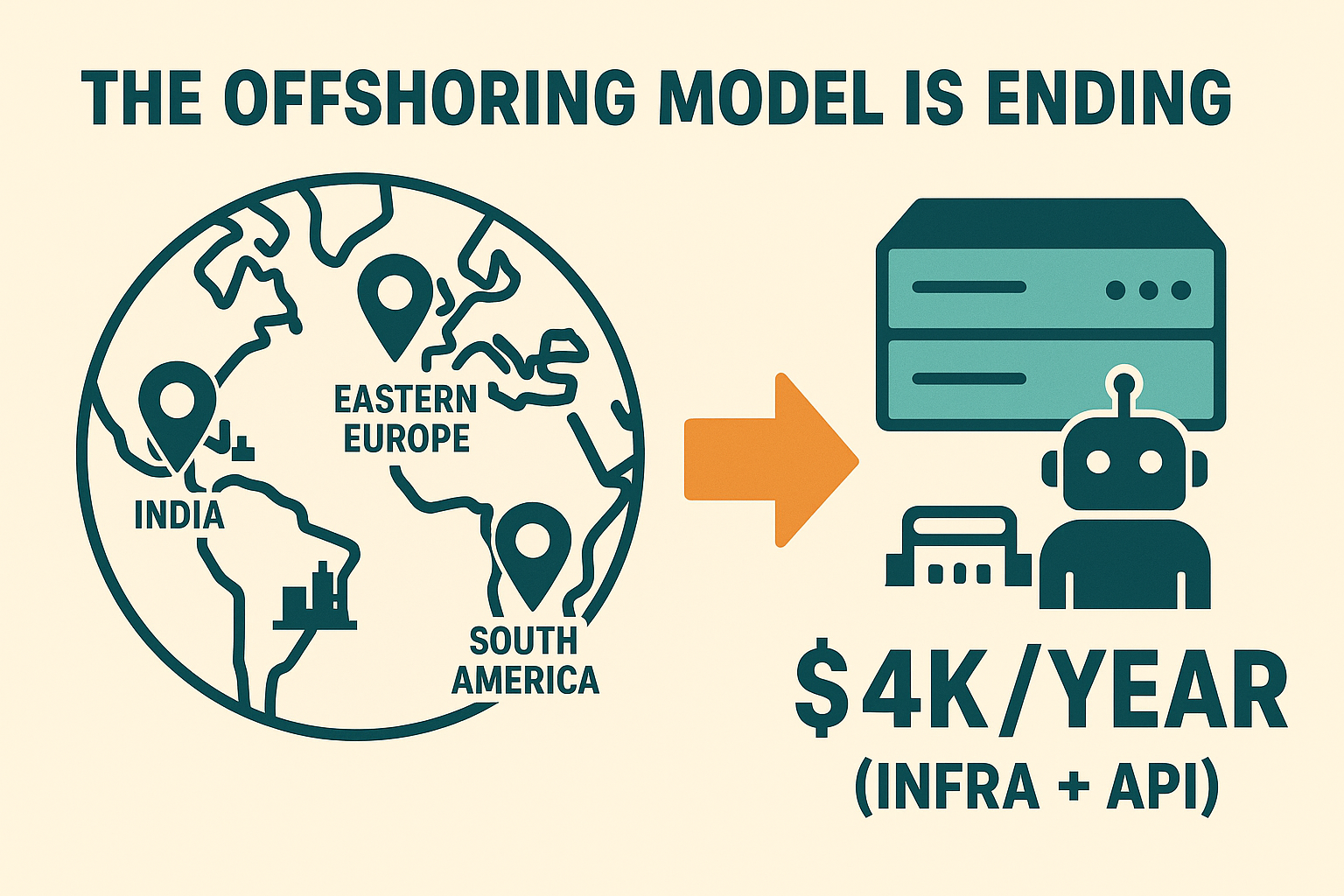

The offshore model works because a human in Bangalore costs one-third to one-fifth of a human in Boston. But agents don't have a geography.

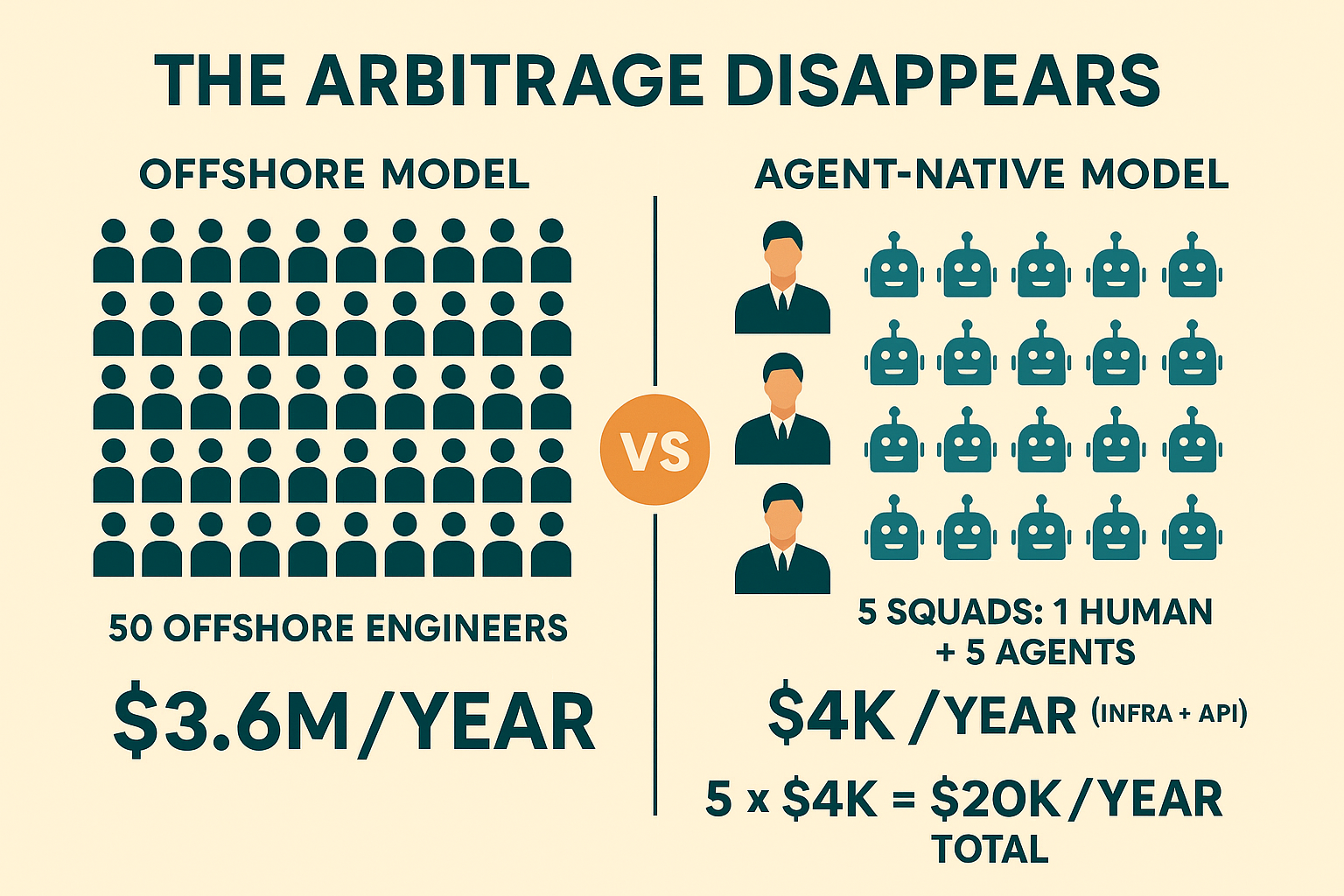

The cost of an agent doing maintenance work, bug fixes, ticket resolution, testing, documentation: near-zero marginal cost after infrastructure. A 50-person offshore team across India, Eastern Europe, or South America at $35/hour costs roughly $3.6M per year. The agent-native equivalent: one human per squad, managing 5-7 agents. Five squads, $4K/year all-in (infrastructure + API costs). Twenty thousand dollars total. The arbitrage doesn't narrow. It disappears.

The same $25/month VPS I described in OpenClaw: The Elephant in the Room, the one that replaces your SaaS subscriptions, replaces your offshore team too. Same server. Same agent orchestrator. Different budget line being zeroed out. The SaaSpocalypse and the offshoring collapse aren't separate stories. They're the same disruption hitting different line items on the same P&L.

This is where the PE math flips completely. "Buy company, offshore team, improve EBITDA" was the playbook for a decade. The new version: "Buy company, deploy agent infrastructure, collapse operational costs." Same thesis at the strategic level, cost optimization driving EBITDA improvement driving higher exit multiple. Radically different execution. And radically different winners.

The Shift-Left Gut Punch

There's a deeper layer to this that goes beyond cost. Offshoring didn't just move work to cheaper geographies. It added layers.

Business user to product manager to onshore tech lead to offshore team lead to offshore developers to QA and back up the chain. Six handoffs for a dashboard change. I lived this for twenty-five years. I watched requirements get garbled crossing time zones, context evaporating at every handoff, simple feature requests turning into three-month projects because the people who understood the problem were separated from the people writing the code by an ocean and four management layers.

Half the coordination overhead existed because we separated the people who understand the problem from the people writing the code. Agents don't have that problem. They live in the context.

The shift-left pattern I explored in Back to the 90s is the other half of the pincer movement. Business users are reclaiming technology. When a finance controller can tell an agent what they need and the agent builds it, the entire intermediary stack collapses. Not just the expensive onshore half. All of it. The offshore team, the onshore coordination layer, the project managers tracking progress across time zones, the tech leads translating requirements into Jira tickets that get mistranslated back into code.

Agents don't just do the work cheaper than an offshore team. They eliminate the reason the offshore team structure existed in the first place: the gap between intent and execution. When the agent lives in the codebase, when it understands the business rules, when it can ask the user a clarifying question in real time instead of waiting for tomorrow's standup call across nine time zones, there's nothing to translate. Nothing to hand off. Nothing to lose in transit.

What the Giants Are Doing (And Why It Won't Save Them)

The IT services companies aren't blind. They see what's coming. Look at what they're doing.

TCS claims 217,000 employees with "advanced AI skills" and $1.8B in AI revenue. They're also cutting 2% of mid-level and senior employees while hiring AI-native freshers at the bottom. Infosys has 275,000 employees AI-certified and just signed a partnership with Anthropic for agentic AI in regulated industries. Wipro declared itself an "AI-first firm," committed $1B over three years, and launched an outcome-based billing model. Cognizant's own internal report admits 93% of jobs will be affected by AI, impact "faster than expected." They launched an "AI Factory" in March 2026.

Massive investments. Aggressive pivots. Every earnings call heavy with AI talking points.

But here's the fundamental problem: they're trying to sell AI services using the same headcount-based billing model that AI is about to destroy. "We'll send you 50 AI engineers instead of 50 Java engineers." That misses the point entirely. The whole value proposition of agents is that you don't need 50 people. You need 5 people and 50 agents. The IT services model doesn't survive the transition from selling hours to selling outcomes.

Wipro's shift to outcome-based billing is the most honest acknowledgment I've seen. But moving from billing hours to billing outcomes means your revenue is no longer a function of headcount. Which means your 250,000-person workforce isn't an asset. It's a liability. That's the trap. You can't gradually transition a model that depends on human volume to a model that explicitly eliminates human volume. It's not a pivot. It's a metamorphosis. And most caterpillars don't survive it.

The same dynamic hits the staffing companies. Randstad Tech, Hays, ManpowerGroup's tech placement divisions. Their model is pure volume: place contractors, bill a markup on their hourly rate. When agent infrastructure replaces the demand for those contractors, there's no pivot available. You can't place agents through a staffing firm. You can't bill markup on a VPS. The entire contracting company business model, billions in annual revenue, depends on employers needing humans they can't find or don't want to hire permanently. Agents collapse both sides of that equation.

The New Playbook

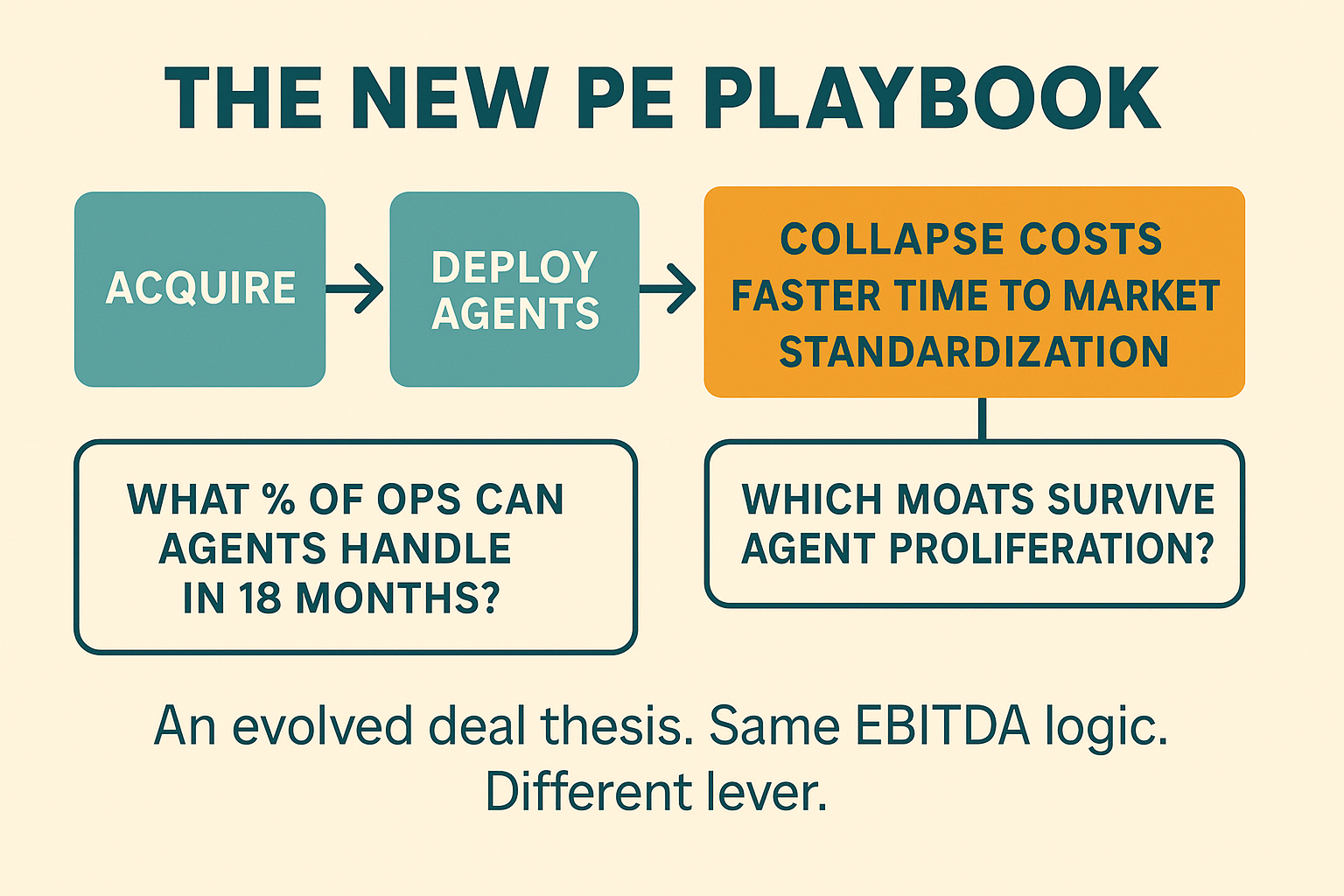

For PE operating partners, the thesis update is straightforward even if the execution isn't. Stop underwriting deals on offshore labor arbitrage. Start underwriting on agent-readiness. The cost optimization lever hasn't disappeared. It's changed form.

The companies that deploy agent-native operations first will compress costs faster than any offshoring initiative ever could. No six-month ramp-up. No 30% annual attrition to manage. No cultural integration workshops. No timezone arithmetic. The deal memo should ask: what percentage of this company's operations can be handled by agents within 18 months? That's your new EBITDA improvement slide. That's the number your exit multiple depends on.

For public equity investors, the signal is the same one I described in the SaaSpocalypse piece. Watch which companies credibly transition to agent-native operations. Not which ones announce AI partnerships at Davos. Not which ones rebrand their offshore delivery center as an "AI Center of Excellence." Which ones actually reduce headcount while maintaining or increasing output. That's the only metric that matters.

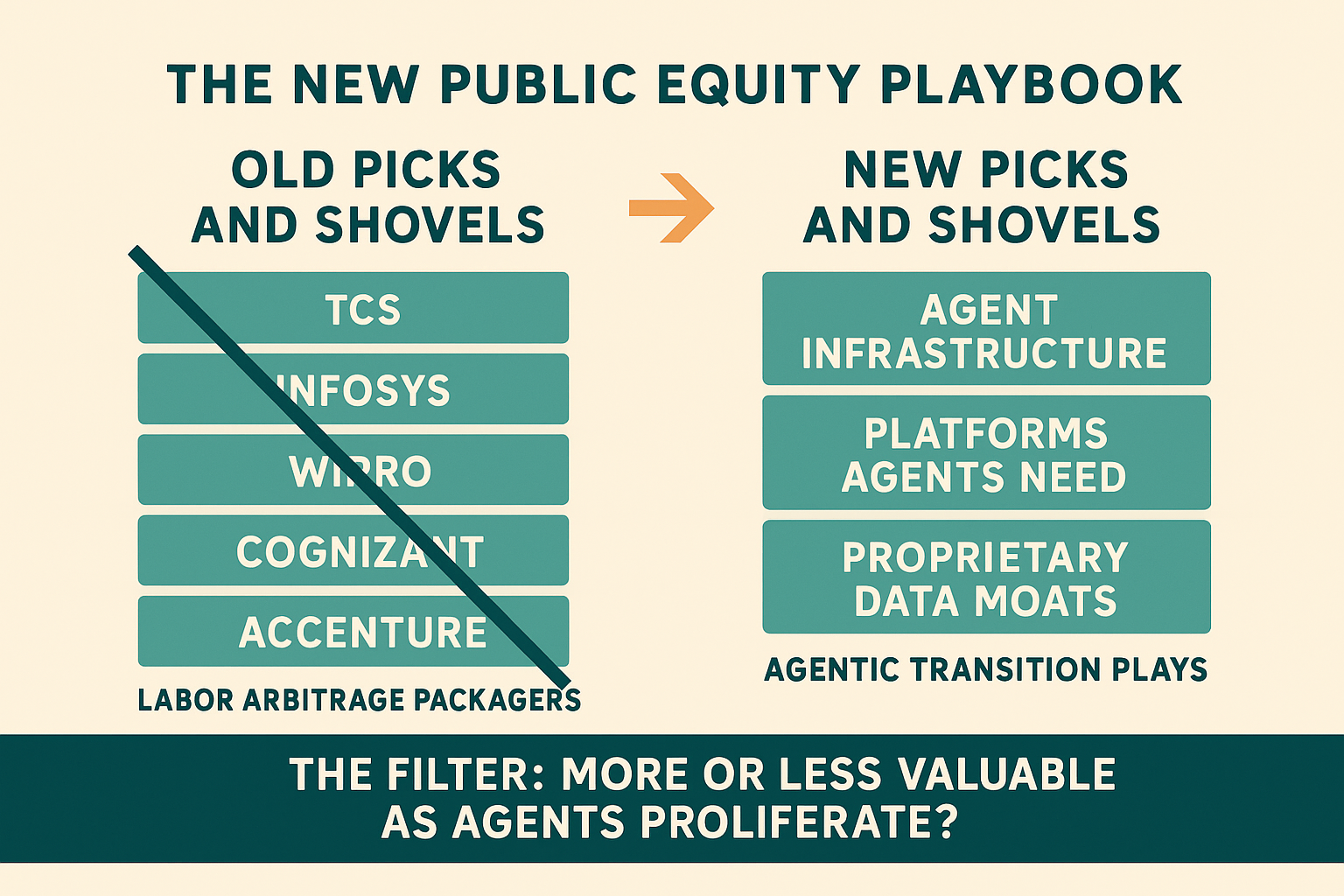

The old picks-and-shovels were TCS, Infosys, Wipro. The companies that packaged labor arbitrage as a service. The new picks-and-shovels are the agent infrastructure providers. Different names, different P&Ls, same structural position in the value chain. The investment question shifts from "which companies are offshoring efficiently?" to "which companies are going agent-native fast enough?"

The Three-Year Clock

I'm not saying offshore teams disappear Monday. I am saying the economic model underneath them is collapsing in plain sight.

You'll still need humans for judgment, architecture, client relationships, complex problem-solving. The 80% of offshore work that's ticket-driven, well-defined, and repetitive? That's exactly what agents do best.

The transition isn't slash-and-burn. It's organic compression. Every open headcount goes through the filter: can an agent do this? Every offshore contract renewal gets scrutinized against agent alternatives. The Klarna lesson applies: move thoughtfully, but move now. Klarna's AI assistant, launched in February 2024, handled the workload equivalent of 700 full-time customer service agents within its first month, managing 2.3 million conversations across 35 languages — and the company projected a $40M profit improvement for the year as a result (Klarna press release; Forbes, March 2024). The companies that figure out agent-native operations first will command premium multiples. The ones still running 200-person offshore teams in 2028 will be the Kodaks of this cycle.

If you're a PE firm still underwriting deals on offshore labor arbitrage in 2026, you're underwriting on an assumption with a three-year expiration date. If you're a public equity investor holding IT services names as "operational efficiency" plays, you're watching the efficiency disappear in real time. $56 billion in market cap says the market agrees.

The investors who rewire their thesis in 2026 and 2027 will capture the next cycle. The ones who wait for certainty will be writing down positions.

Twenty years ago, I helped build the offshoring model because it was the best tool available. Today, better tools exist. The question isn't whether the model changes. It's whether you're positioned for what comes next.

The Agentic-Native Company

The offshoring model solved a cost problem by moving work to cheaper geographies. The agentic-native company solves the same cost problem differently — by eliminating the work-as-headcount equation entirely.

In the agentic-native company, the Global Delivery Model isn't a team in India or Eastern Europe. It's an agent infrastructure running 24/7 on owned hardware. The economies of scale I spent years extracting from offshore consolidation are built into the architecture by default. No attrition. No time zone arithmetic. No coordination overhead. The governance model, the capability boundaries, the audit trails — all codified in configuration files, not management layers.

This isn't a cost-cutting story. It's a structural redesign. The PE operators who understood that centralizing offshore delivery was the real value lever — not just the arbitrage, but the scale — will understand this transition fastest. The mechanics are identical. The lever is different.

Most organizations know the thesis. Few have built the execution model. The gap between understanding that agents will reshape operations and actually deploying agent-native infrastructure across real business processes — that's where the work lives. Knowing what to automate first, how to structure the human-agent boundary, how to govern capability without strangling velocity.

I've spent one year building this, running it, and documenting what works. That's what Agentic Native is: ground-level practitioner knowledge for the organizations navigating this transition.