By Aymeric Gerardin

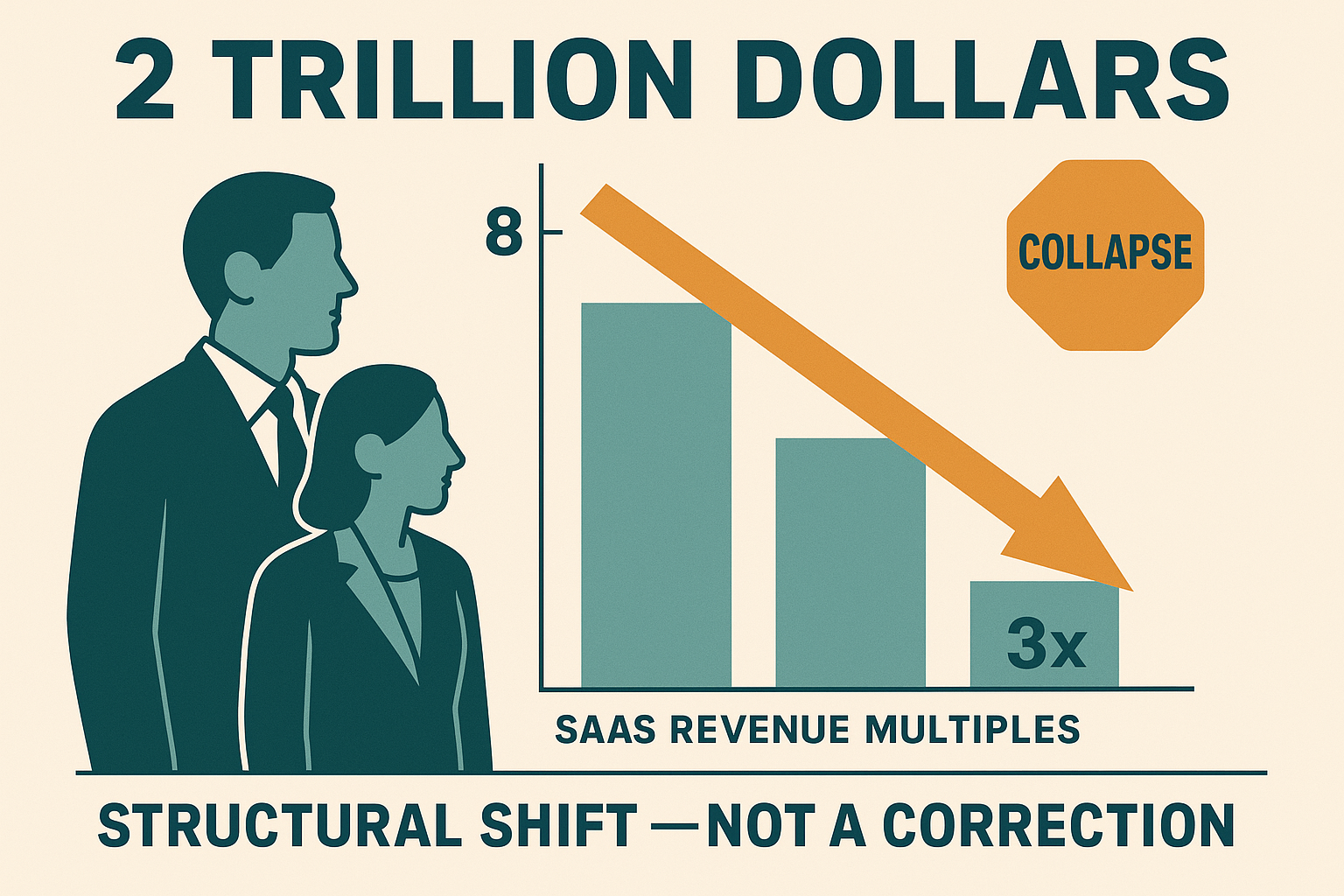

Two Trillion Dollars

Roughly $2 trillion in SaaS market cap has evaporated since the start of 2026. Median revenue multiples fell from 7-8x to 3-4x. Forward earnings multiples compressed from 39x to 21x in months. Atlassian reported its first-ever enterprise seat decline. Salesforce, ServiceNow, HubSpot: all bleeding.

This isn't a correction. Corrections recover. This is structural.

Autonomous agents are collapsing the cost of building software toward zero. Every SaaS company whose value proposition boils down to "we built this so you don't have to" now has an existential problem. I'm watching it from a perspective most analysts don't have: a private investor who tracks public equity closely, and a practitioner who actually builds with the systems doing the damage.

Most investors still don't understand how exposed they are.

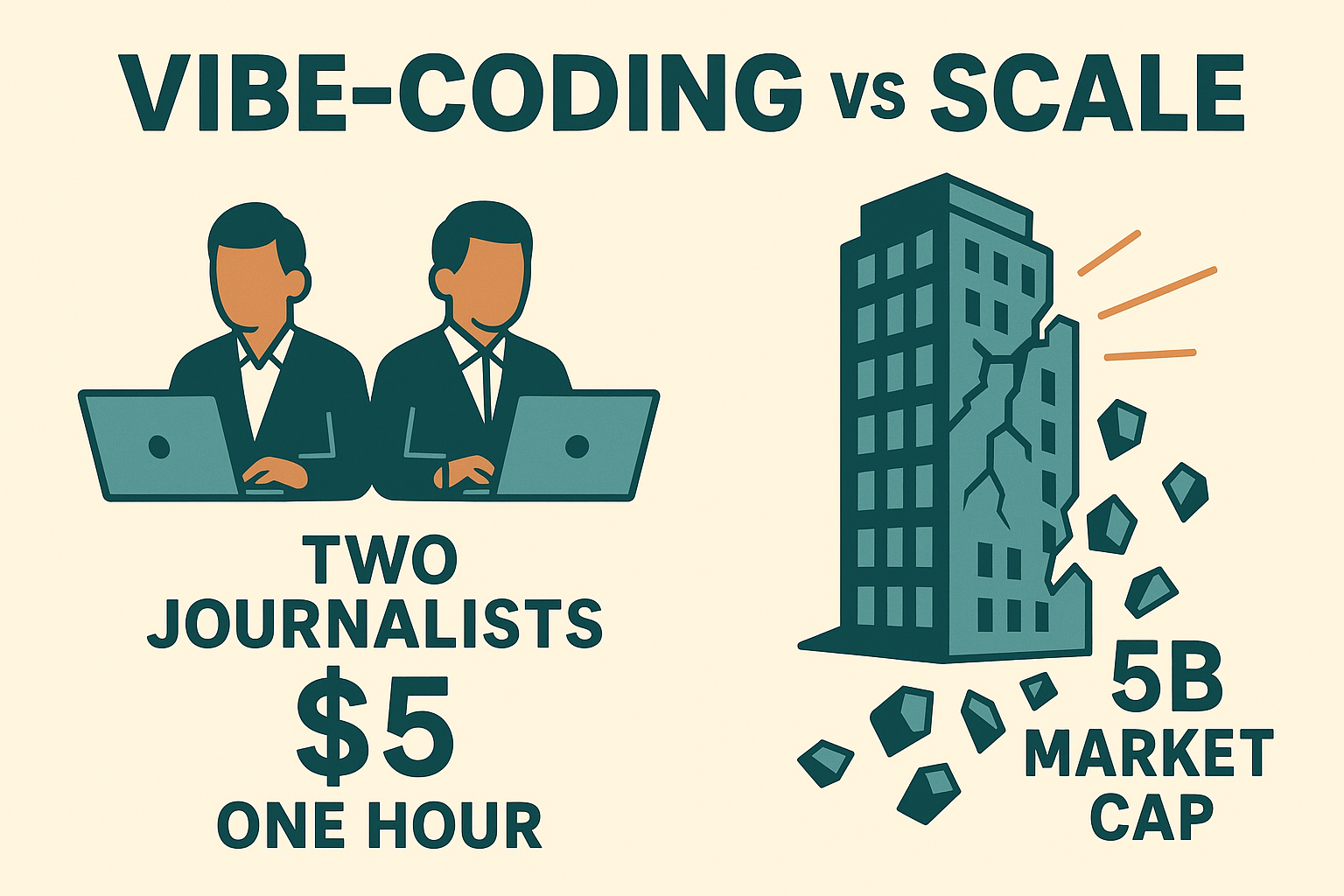

The Monday.com Moment

Two journalists. Zero coding experience. Under an hour. Five dollars in compute.

CNBC's Deidre Bosa and Steve Kovach used Anthropic's Claude Code to build a Monday.com clone (https://www.cnbc.com/2026/02/05/how-exposed-are-software-stocks-to-ai-tools-we-tested-vibe-coding.html). They asked it for a project management dashboard with multiple boards, assigned team members, and status controls. It produced a working prototype in minutes.

Then they pushed further. They asked Claude to research Monday.com on its own, identify the core features, and recreate them. It added a calendar. They connected the clone to email and turned it into a personalized project manager. The system found a forgotten birthday invite, added reminders to book travel, and flagged a waiver that still needed signing.

Monday.com's market cap: $5 billion.

And the Silicon Valley insiders CNBC interviewed named the same cluster of vulnerable companies: Atlassian, Adobe, HubSpot, Zendesk, Smartsheet. Software that sits on top of work instead of being core infrastructure.

The question every investor should be asking is brutally simple: could an autonomous agent replicate this product in a weekend?

That is no longer a product curiosity. It is the first due diligence question. Before you model growth, before you debate GTM efficiency, before you talk about expansion revenue, you need to know whether the product itself is being commoditized by agentic coding. If the answer is "probably," then whatever you paid at 7x or 8x revenue was based on assumptions that no longer hold.

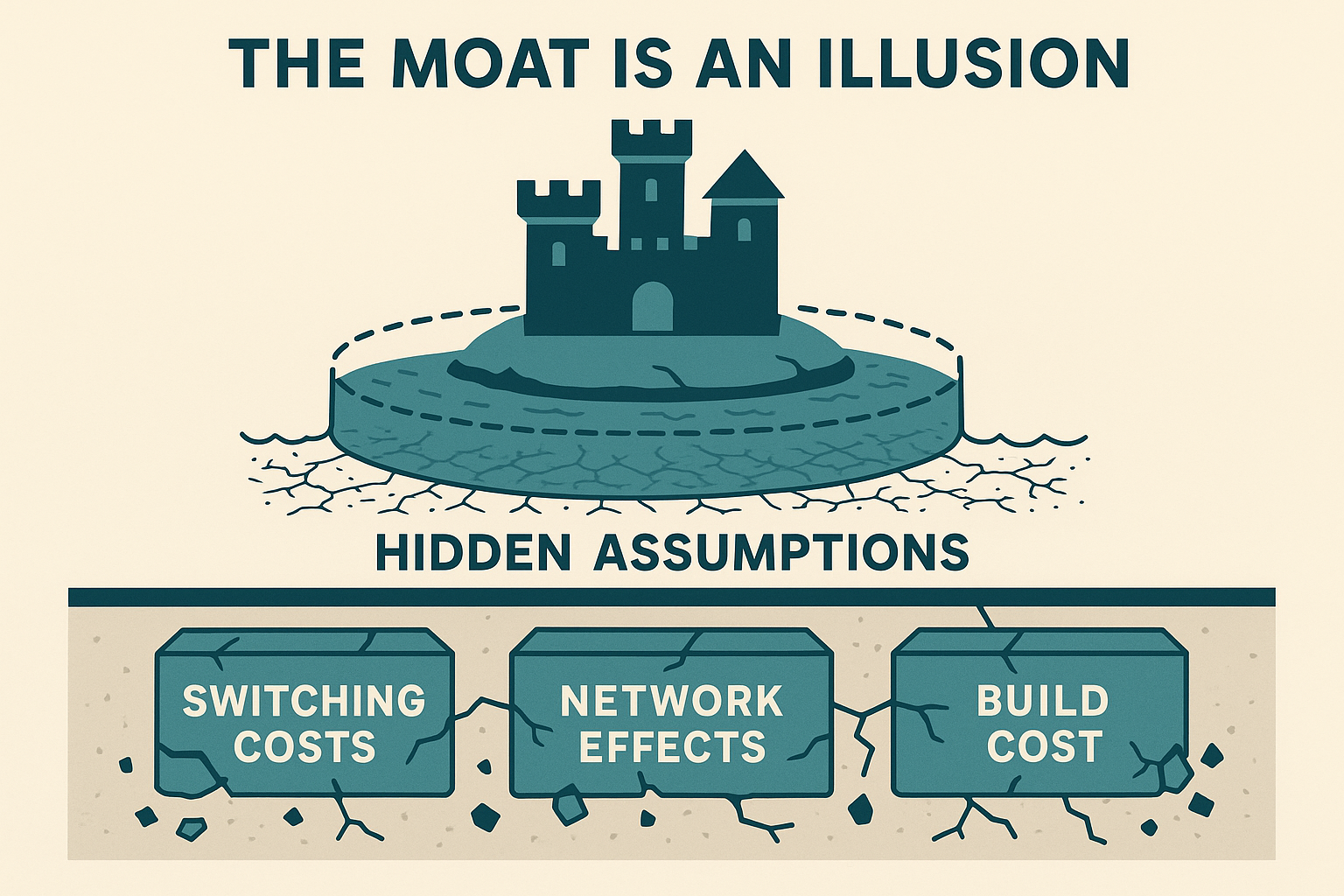

Why Moats Are Failing

Every competitive moat rests on hidden assumptions about what must remain expensive, difficult, or human. AI stress-tests all of those assumptions simultaneously. (Ringstone's Kari Dempsey published a sharp analysis of this pattern: https://www.ringstonetech.com/post/ai-moat-assumptions)

Moats defend against competitors playing the same game. They don't defend against technologies that change the game entirely. Shutterstock had a textbook moat: network effects, scale economies, switching costs. Stock dropped roughly 75%. Not because a competitor beat them. Generative AI collapsed image creation costs to near zero. The economics underneath the moat simply ceased to exist.

The same pattern is playing out across SaaS. When agents can build a project management tool in an afternoon, network effects don't matter. When agents can spin up a CRM from scratch, switching costs don't matter. Klarna replaced Salesforce CRM with an internal AI system. A Base44 customer terminated a $350,000-per-year Salesforce contract and replaced it with a custom AI-powered solution. A Fortune 50 company's leaked internal memo revealed plans to cut Salesforce and ServiceNow license spend by 60%.

That's not competition. That's category extinction.

Speed Compression

Kodak had 15 years to respond to digital photography. They saw it coming. They even invented the digital camera. Fifteen years of runway, and they still couldn't pivot fast enough.

Nokia had 6 years after the iPhone launched. Six years of knowing exactly what was happening, and they still went from market leader to irrelevant.

SaaS companies have maybe 18 months.

The classic innovator's dilemma used to play out over a decade. You could see disruption coming, form a committee, commission a strategy review, pilot something small, iterate, eventually transform. That playbook assumed you had time. AI compresses disruption timelines so severely that traditional strategic planning cycles cannot keep up.

Eighteen months sounds like plenty. It isn't.

A typical enterprise transformation takes 12-24 months just to get through planning and procurement. The companies that start now might make it. The companies that wait for Q3 board approval are already behind.

What This Means for Public Equity

Public equity already started the repricing. Multiples compressed. Narratives broke. Stocks reset lower as investors realized that parts of SaaS were no longer scarce in the way the old model required.

Where the market concluded that the core workflow could be rebuilt faster, cheaper, and with acceptable quality by agents, it already priced in downside in both valuation and expectations.

The signal was straightforward: lower pricing power, weaker seat expansion, worse retention over time, and a structurally lower multiple. The question was never whether a company had AI features. It was whether agentic systems made the product itself less defensible.

What This Means for PE

PE has a much simpler problem than it wants to admit: many portfolios were underwritten on assumptions that no longer hold. If an agent can replicate the core workflow, your asset is not competing only against peers. It is competing against the collapsing cost of software creation.

That makes agentic exposure the first diligence question, not a later technical appendix.

Traditional diligence still covers the usual metrics. Fine. It still misses the issue that now matters most: can agents delete the value of this product faster than management can transform it?

That is the sequence. First, run the right internal due diligence. Then decide the move: rebuild around agents, reposition into a more defensible layer, change pricing and roadmap fast, or accept a lower exit outcome. Every quarter you wait burns value.

What This Means for VC

For startup funding, the shift is already visible. In YC's Spring 2025 batch, 67 of 144 startups, or 46%, were AI agent companies. That is not noise. It is a directional signal. And the demand side is reinforcing it: Menlo Ventures estimated $37 billion of enterprise generative AI spend in 2025, including $18 billion in infrastructure.

The filter is now brutally simple: is this startup building a product that agents will commoditize, or a position that the agentic-working wave will strengthen?

If it is the first, funding gets harder because investors can already see the future customer objection: why buy this as SaaS if I can build enough of it with agents? If it is the second, the company sits in the layers the new model needs: infrastructure, tooling, orchestration, governance, or any startup concept that directly supports the rise of agentic working. That is where startup capital now has a reason to concentrate.

The Agentic-Native Company

The real shift is not adding more AI features to the old software playbook. It is building the internal due diligence muscle to measure agentic value-deletion exposure honestly. Where does agentic AI erase product scarcity? Where does it compress pricing power? Where does it weaken retention, expansion, or the logic behind the moat? If you cannot answer those questions clearly, you do not have the right picture.

That picture has to come first. Only then can investors and executives make the right next move: protect the current asset, reposition product strategy, reset CAPEX allocation, rebuild around agentic leverage, and stop pretending the old playbook still works.

That is the authority the next market cycle will reward. Not the loudest AI narrative. The clearest judgment about where agentic AI destroys value, where it creates leverage and opportunity, and what operating model a company has to build next to capture it. That is the territory where the agentic-native company operates.

What Comes Next

This article focused on the diagnosis. The next part will focus on what to do: where smart capital should move, what to underwrite differently, and how the operating model changes when you take the agentic-native shift seriously.